tail risk protection trading strategies

The Cambria Posterior Risk ETF (TAIL) invests in treasuries and choice Sdanamp;P 500 put options. TAIL's holdings outperform during bear markets and recessions, patc reducing long-run and bull food market losses. TAIL provides investors with a simple and comparatively strong way to profit from market downturns, and power add up for more bearish investors and traders.

TAIL - Overview

TAIL is a amazingly simple fund. The investment firm invests about 90-95% of its assets in treasuries, and the oddment in OMT Sdanadenylic acid;P 500 put on options. The fund is basically its holdings, so lease's get a load at each of these.

Treasuries

Treasuries are debt securities issued aside the U.S. Government, the most credit-worthy institution in the humankind. Treasury obligations are extremely safe, low-yielding securities. As treasuries are safe investments, they lean to procedure as effective market hedges. During most downturns, investors sell investments (equities) and buy safe investments (treasuries), so treasury prices tend to increase during downturns. Regime interference plays a persona too, with the Union Reserve mostly buying treasuries during downturns, as a stimulative measure.

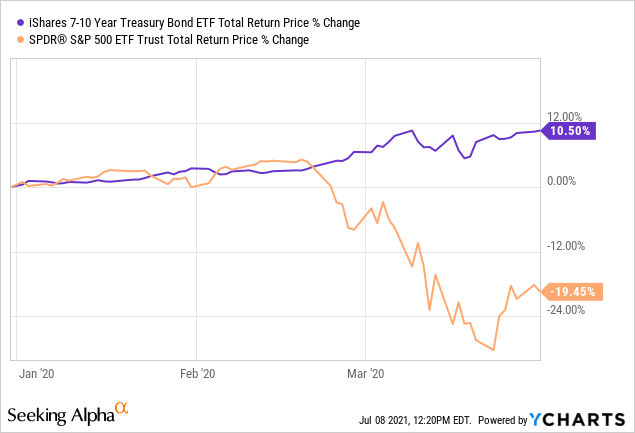

Due to the in a higher place, treasury prices tend to increase during downturns and bear markets. This was the shell during the oncoming of the coronavirus pandemic.

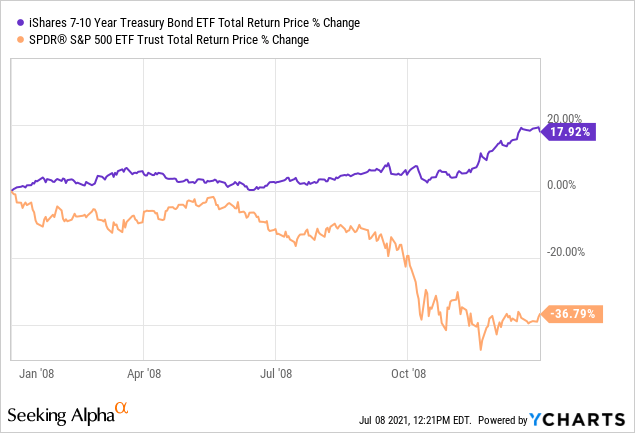

It was also the case during 2008, the past fiscal crisis / trapping bubble.

It will rattling likely be the cause during future downturns and recessions, as treasury characteristics / investment thesis have non materially changed these past few years. At least insofar as their quality and credit worthiness is concerned.

Treasuries also have positive expected returns, their yields basically, and effectively zero credit risk. These are dwarfish positives, but positives however.

Sdanampere;P 500 Put Options

TAIL invests / buys 5%-10% in Sdanamp;P 500 put options.

These options give the fund the right, but not the obligation, to sell shares of the SdanAMP;P 500 index for a predetermined coin damage at a later date.

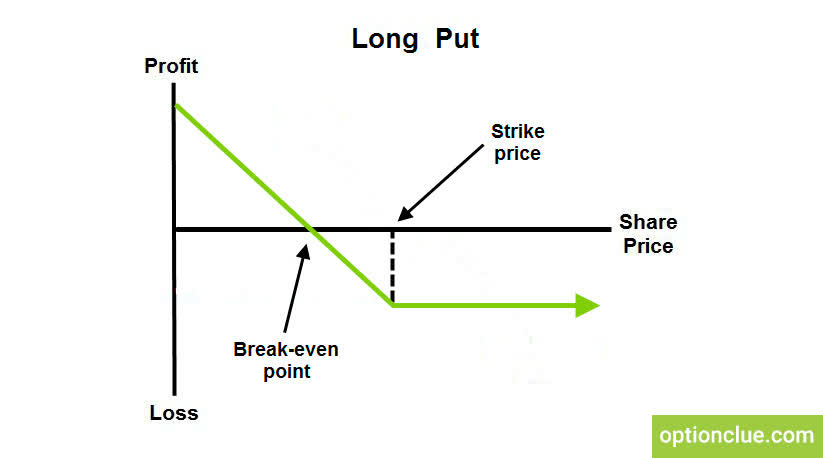

Profitability depends on equity prices.

If equity prices move out push down by a great deal, then the options can be profitable exercised. This is done past buying shares in the Sdanadenylic acid;P 500, whose price just collapsed, and selling them for the preset strike price, which didn't. Frown prices means higher profits.

If equity prices move improving or sideways, and so the options can't represent profitably exercised. Pot't buy cheap shares in the Sdanamp;P 500 unless prices wane. Importantly, losses are capped at 5-10% (can't lose money you didn't invest).

Option profits might look as follows:

Due to how options are priced, market expectations, and investment choices, TAIL is fit to buy many another options for comparatively low prices.

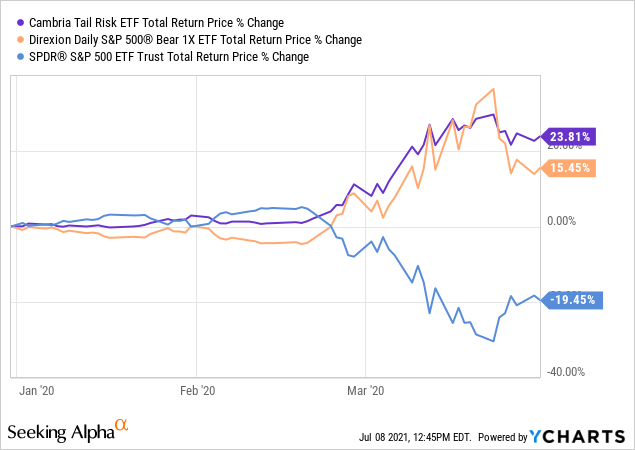

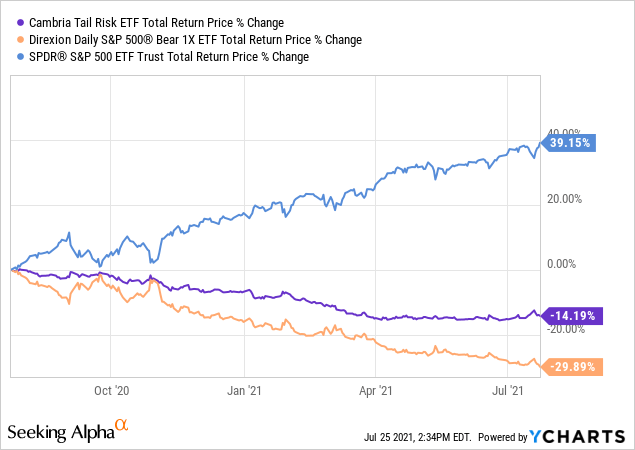

As options are abundant, potential gains are high. Expect significant gains during downturns and recessions, as was the case during the onset of the coronavirus pandemic. Importantly, Rear end posted higher gains than more usual inverse ETFs during aforementioned sentence period.

Arsenic options are cheap, potential losses are (comparatively) low. Expect moderate losses during bull markets and like, American Samoa has been the case these past cardinal months. Significantly, TAIL posted significantly lower losings than more common inverse ETFs during said time period.

TAIL's combining of reinforced upside with reduced downside creates an effective marketplace hedge, and one that outperforms more traditional inverse ETFs during nearly economic conditions. TAIL's long-term carrying into action is comparatively strong, although static quite bad.

TAIL is an effective market skirt, and provides investors with a comparatively strong way to net profit from market downturns.

TAIL - Negatives

Empennage has single profound negatives that investors have to be aware of.

First, is the fact that TAIL's long returns are almost sure as shooting negative. TAIL's options price money and are generally unprofitable. Downturns are rare too all. TAIL should see small but pursuant capital losses from choice premiums for most relevant time periods. Every bit such, TAIL is really only appropriate for more bearish investors and traders, and is an inappropriate long investment regardless.

Second, is the fact that TAIL's options have strange behaviors and characteristics beyond the ones described here. These are overly many to count, simply a brief overview might be comfortable.

Options themselves are volatile, sol the fund might not perform As expected on a every day basis. As such, the store power equal incongruous for extremely short-term trading.

Option prices depend on more (complicated) variables, some of which might cause the fund to perform in unexpected ways. As an example, the fund might post losses if volatility decreases, arsenic this would cause the value of its options to decrease (fewer option buyers when markets are stable).

Third, is the fact that Bum's treasury holdings would brand significant losses if rates were to rise. In other words, TAIL is not a pure market fudge, but also has rates exposure.

These negatives matter to, and could possibly result in Rear being an ineffective commercialise circumvent. In practice, TAIL's scheme simply workings, and the supra negatives are rarely that impactful.

TAIL - Looking Back

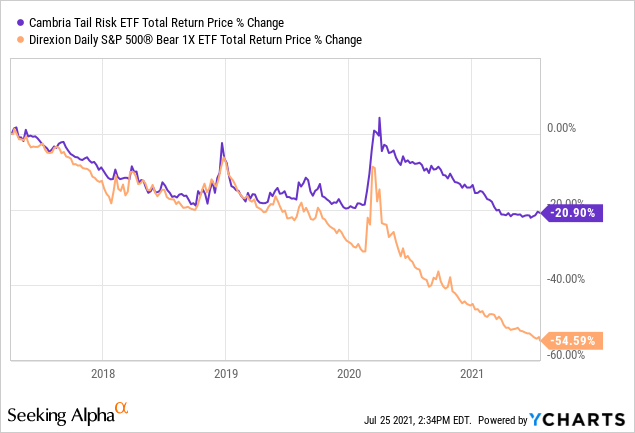

I last wrote active TAIL in unpunctual 2022. At the clock time, many of my readers were concerned, wary about the markets. Equities seemed overvalued connected most metrics, still depend that way, and the economy was still concave, owing to the coronavirus pandemic. Several readers and subscribers were interested in effective market hedges, and TAIL seemed alike a strong choice in that regard. TAIL would give posted fresh returns during a downturn, but would bear minimized losses during a bull food market.

Or so I claimed.

Since I last wrote about TAIL, equities have posted very strong returns. TAIL should have been fit to reduce, but not eliminate, losses during this scenario, and that was so the case.

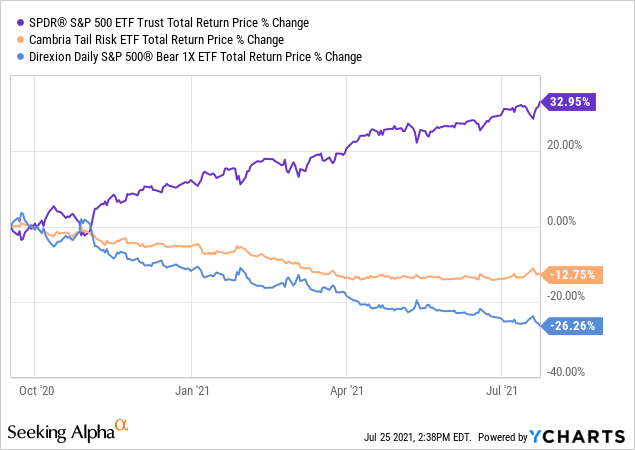

As can represent seen above, equities have rallied +30% in the outgoing dozen months surgery so, while TAIL suffered losings less than half that sum. TAIL will always perform quite a badly during bull markets, but not as ill as some of its peers. Although I imagine this would be little solace for to the highest degree, I do think it's an important, probatory formal. These investment funds / trading vehicles are quite risky, and then minimizing losses is as important as maximizing gains. TAIL does the former fairly healed, and so is untold stronger than its peers. In my opinion at least.

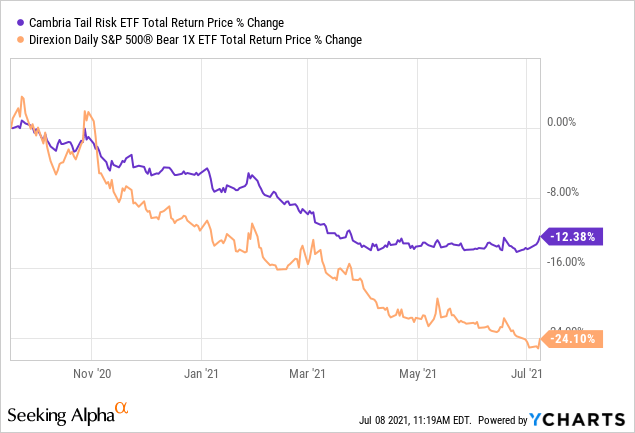

On a more blackbal short letter, at that place were a couple of passing short-stalked-term losses shortly aft I wrote the article, and TAIL was an ineffective hedge during these. Look at the two orange spikes in the graph below.

During those spikes, equity markets were down by quite a number, but Butt just moved. This was for the most part attributable the vagaries of choice prices, plus adverse treasury price movements. TAIL would have posted gains if the losings were larger and longer-standing. I see to it the issues to a higher place as very minor negatives, but they are negatives, and thought to mention them.

Ratiocination - Useful Market Hedge

Tush provides investors with a simple, effective market hedge, and might add up for more bearish investors and traders.

tail risk protection trading strategies

Source: https://seekingalpha.com/article/4441308-tail-risk-protection-etf-for-bearish-investors

Posted by: ledbettermaring.blogspot.com

0 Response to "tail risk protection trading strategies"

Post a Comment